Paper presented at the AfAA 2nd Annual International Arbitration Conference, 15th - 16th April 2021

Executive Summary

Incorporating investor obligations in international investment agreements may serve to achieve a more equitable balance as between the interests of host States and investors in international investment law. This approach has gained considerable traction in Africa. Now, as the project for the African Continental Free Trade Area advances, the question is not whether its investment protocol should contain investor obligations but rather how such obligations might be adopted in the most impactful manner. Beginning from the framework of prior instruments culminating in the draft Pan-African Investment Code of 2016, this article proposes the inclusion of enforceable investor obligations which may be balanced against better-defined investor protections in order to afford greater legal certainty paired with meaningful legal remedy, and thereby to foster expansion of responsible intracontinental investment in Africa.

Investor Obligations in Africa to Date

Identifying an optimal means of balancing the interests of the investor and the host State requires understanding their true interests. While the interest of the investor is to realize (and often to repatriate) a profit under rule of law, the interest of the host State is to enjoy benefits of capital inflows while free from harm. In order to balance these interests, investment agreements may establish not only rights of investors but also their obligations. While perhaps considered novel in some corners of the earth, investor obligations have a rich history in Africa.[2]

Through the nearly five years of the Pan-African Investment Code’s existence, it is by now well known that the Code is declared non-binding. Further than this, it would not itself textually establish arbitral jurisdiction to hear investor-State disputes even if it were binding. Rather, the Code permissively sets out that the African States may consent to such sort of arbitral jurisdiction if they so wish.[3] It is thus little more than a truism, a simple affirmation of an existing and inherent sovereign right.

Looking beyond consent and jurisdiction to the merits, to the substantive rights granted and the obligations that would be imposed under the model of the Code, what one finds is, as measured by the paradigm of global treaty practice over the past half-century, quite extraordinary. That paradigm has been the one-way street, a street in which substantive protections (substantive rights) flow in favor of the investor only. But when one looks to the Code, one sees two things, in rather stark relief.

First, while certain investment protections have been preserved (including the classic protection against expropriation), others which investors have come to expect as a matter of right, first and foremost the guarantee of fair and equitable treatment (“FET”) as well as the guarantee of full protection and security (“FPS”), are nowhere to be found. It is difficult to ignore the irony that by this choice, the African States would deny to investors of their African counterparties guarantees which have been afforded to Northern investors essentially since the time of independence (and which would continue to be afforded to those investors in the absence of any parallel effort to alter or amend still-extant North-South treaties). In a rather perverse manner, it is almost as if intra-African investors would be made to suffer for the African States’ dissatisfaction with a generation’s worth of arbitration results originating in the North and with which they have had nothing to do.

Second, building upon the tradition of the regional economic communities (“RECs”) and other recent intra-African investment instruments,[4] the Code contains investor obligations, thus marking a definitive end to the one-way street. The provisions on investor obligations are perhaps less than fully formulated, but they are more than merely aspirational or preambulatory: they are conceived to be hard investor obligations.[5] In a certain sense, here, the irony deepens. Northern investors may continue to enjoy FET and FPS while being free of any countervailing control on their conduct at international law. Meanwhile, intra-African investors are denied FET and FPS and, not only this, they are saddled with burdensome obligations (or so the argument might go). It has been written that this result is “not a function of animus” but rather “doctrinal confusion.”[6] What is certain is that as measured by these two features, the Code marks a fairly dramatic swing of the pendulum: reduced investor protections paired with inclusion of investor obligations.

This result in the Code is, in large part, a function of the multilateral negotiation dynamic. It may be recalled that as the modern era of international investment law was first being forged in the decade after the Second World War, the multilateral 1959 Draft Convention on Investments Abroad (the so-called Abs-Shawcross initiative) would fail.[7] Meanwhile, the first bilateral investment treaty (the renowned Germany-West Pakistan treaty) was markedly more successful in setting the tone; it was concluded in that same year.[8] It seems evident that the enduring paradigm of bilateral instruments may be explained by elementary negotiation theory: States with greater bargaining power (or the perception or illusion thereof) were able to gain more favorable terms vis-à-vis a single negotiating partner.[9] More powerful States thus preferred this result as contrasted to the less advantageous lowest common denominator which would inevitably emerge in a more rigorous multilateral negotiation.[10] Put more bluntly, capital exporting States were able to gain more favorable terms vis-à-vis capital importing States by playing them one-on-one.

In an illustration of the enduring power of this bilateral paradigm, four decades after the demise of the Abs-Shawcross initiative, an initiative by the OECD for a Multilateral Agreement on Investment would similarly meet with failure when negotiations were discontinued in the late 1990s.[11] Looking forward another twenty years, it is evident that this multilateral negotiation dynamic persists in the present pan-African investment initiatives. The instrument establishing the Continental Free Trade Area is, after all, not merely a multilateral instrument but a sort of mega-multilateral instrument comprising all the African States minus Eritrea.

The result that has been reached in the Code may ultimately contravene the very purpose of that insrument itself, as traceable to venerable prior African instruments. The establishment of the Organisation of African Unity in 1963 may be said to formally mark the birth of the pan-African project.[12] By 1980, when the Lagos Plan of Action for the Economic Development of Africa was adopted, the States clearly indicated their commitment to regional integration.[13] This agenda was furthered in the Treaty Establishing the African Economic Community of 1991,[14] following which many RECs were established. A primary purpose of these instruments was to promote intra-African trade and investment and thereby propel a balanced economic development.[15] The Code was, by its own terms, aimed squarely toward this end.[16]

To tie these strands together: the swinging of the pendulum that is seen in the Code reflects an element of backlash against the status quo of the investment law régime, dissatisfaction with the investment law jurisprudence, to be sure. But this result portends deep dissatisfaction paired with the reality of the mega-multilateral negotiation dynamic. We have today vastly uneven levels of economic development and capital accumulation across and within the very many African States. This reality leads to competing objectives and interests in the crafting of a pan-African brand of international investment law.

The bad news is that a poor historical record in the seeking of multilateral investment agreements now forms the backdrop against which the investment protocol initiative unfolds. The good news is that if we honestly acknowledge and confront this challenge, there may be a solution that presents itself.

The Prospect of Balance in the Investment Protocol of the African Continental Free Trade Area

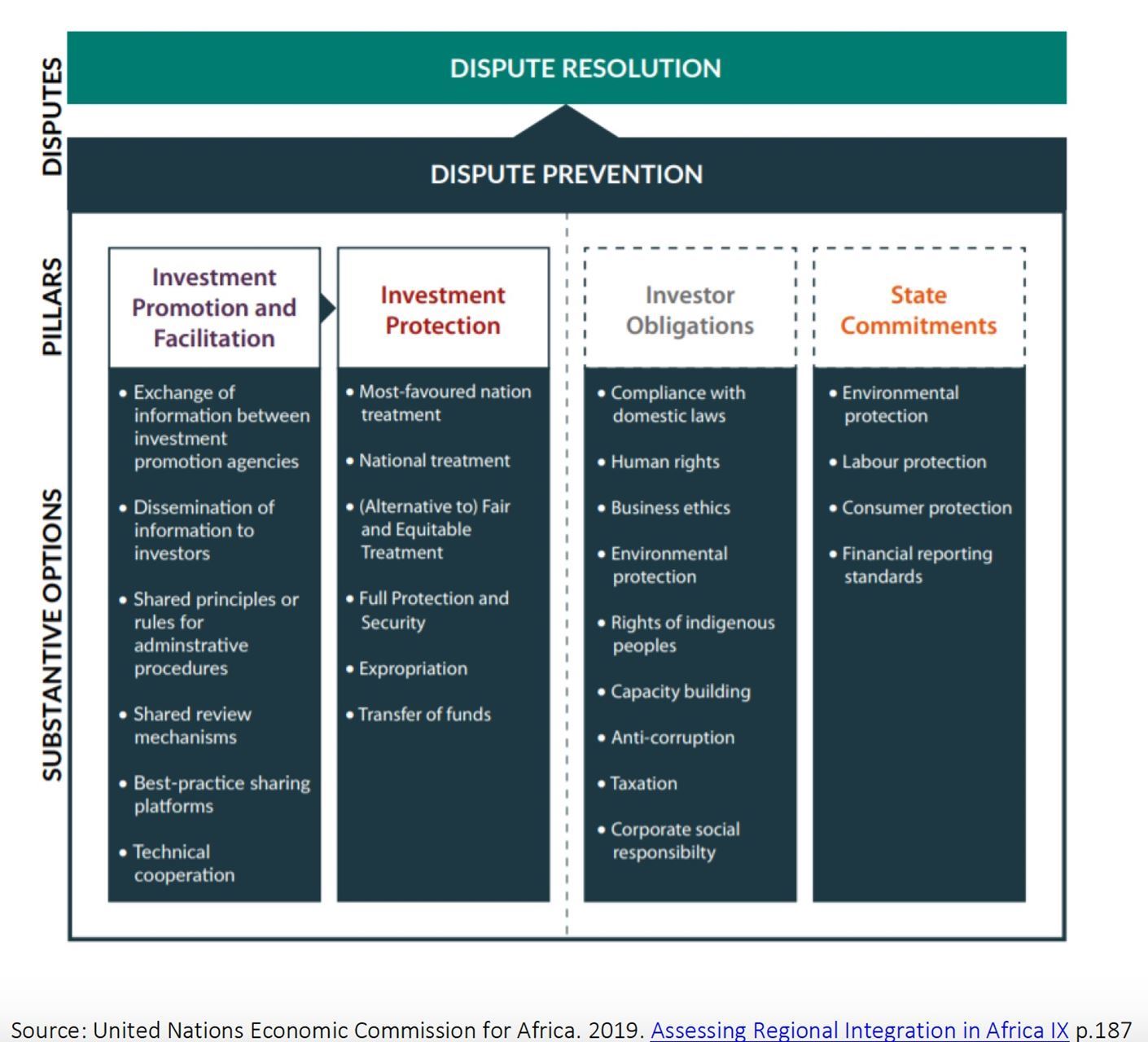

The Agreement Establishing the African Continental Free Trade Area came into effect on 30 May 2019.[17] Within a July 2019 joint report of the United Nations Economic Commission for Africa, the African Union, the African Development Bank, and the United Nations Commission on Trade and Development entitled Assessing Regional Integration in Africa IX (“ARIA IX”), the authors offer four pillars of a foundation for its investment protocol.[18] These four pillars are now adopted as underpinning the forthcoming investment protocol negotiations, including a pillar of Investor Obligations:

United Nations Economic Commission for Africa et al, Assessing Regional Integration in Africa IX (2019) 187

One also sees in this depiction an Investment Protection pillar, including reference to FET (or a possible alternative thereto). Further, one sees a first pillar of Investment Promotion and Facilitation (which items are often foremost in investors’ minds at the time of making an investment) as well as a final pillar of State Commitments (which rightfully calls upon the States to do their part in achieving the goals of sustainable development).

Each of these pillars carries the potentiality of transformative power that may be unleashed to expand responsible intra-African investment. The focus for purposes of the present article is upon the second and third pillars, for the fundamental suggestion is that perhaps the pathway forward in first reaching a mutually agreeable instrument and thereby advancing intra-African investment lies in seeking an optimal point of balance as between investor rights and obligations. This objective requires going beyond merely setting out in a meaningful way the host State’s right to regulate.[19] It rather requires hard investor obligations that are actually justiciable in the investment arbitration forum.[20]

As may be seen in the Code, Africa has now spoken in favor of the enfranchisement of investor obligations. This approach is also gaining acknowledgement in the context of other fora, including more universal efforts for the reform of international investment law. Thus, the UNCITRAL Secretariat has recorded that its Working Group III for Investor-State Dispute Settlement Reform “may wish to consider formulating provisions on investor obligations which would form the basis for a State’s counterclaims” and that such obligations “may relate to the protection of human rights and the environment, compliance with domestic law, measures against corruption and the promotion of sustainable development.”[21] The Institut de Droit International has, for its part, recorded by resolution that “[b]oth the State and the investor are equally entitled to submit a claim in relation to an investment to a tribunal, subject to the terms of the instrument of consent, interpreted in accordance with the principle of the equality of the parties,” this latter being “a fundamental element of the rule of law that ensures a fair system of adjudication” and, as such, “a general principle of law applicable to the procedure of international courts and tribunals.”[22] Within the very most recent workplan document of the Working Group III, the point is affirmed once again, it being noted that its scope of works shall include “consideration of new rules with respect to… counterclaims.”[23]

Having witnessed the pendulum swing of the Code, reduced investor protections and expanded investor obligations, one manner of propelling the investment protocol of the Continental Free Trade Area may be to let the pendulum fall to the center of gravity, to seek a truly fair and equitable balance of investor rights and obligations.

On investor protections, reaching back to FET, it might be re-incorporated in a manner so as to afford greater legal certainty than one presently enjoys at the status quo. On this point, Africa faces a vast spectrum of options, perhaps beginning from a simple express prescription that FET is to be equated to the minimum standard of treatment of aliens at customary international law. This has been done in the context of, for example, the 2001 note of interpretation rendered by NAFTA’s Free Trade Commission and intended thereafter to be binding in disputes under NAFTA.[24] The formulation was then adopted in the 2004 US model treaty and maintained in the 2012 model treaty:

“1. Each Party shall accord to covered investments treatment in accordance with customary international law, including fair and equitable treatment and full protection and security.

2. For greater certainty, paragraph 1 prescribes the customary international law minimum standard of treatment of aliens as the minimum standard of treatment to be afforded to covered investments. The concepts of ‘fair and equitable treatment’ and ‘full protection and security’ do not require treatment in addition to or beyond that which is required by that standard, and do not create additional substantive rights. The obligation in paragraph 1 to provide:

(a) ‘fair and equitable treatment’ includes the obligation not to deny justice in criminal, civil, or administrative adjudicatory proceedings in accordance with the principle of due process embodied in the principal legal systems of the world; and

(b) ‘full protection and security’ requires each Party to provide the level of police protection required under customary international law.”[25]

In 2007, the drafters of the Common Market for Eastern and Southern Africa investment agreement employed a perhaps functionally equivalent formulation:

“1. Member States shall accord fair and equitable treatment to COMESA investors and their investments, in accordance with customary international law. Fair and equitable treatment includes the obligation not to deny justice in criminal, civil, or administrative adjudicatory proceedings in accordance with the principle of due process embodied in the principal legal systems of the world.

2. Paragraph 1 of this Article prescribes the customary international law minimum standard of treatment of aliens as the minimum standard of treatment to be afforded to covered investments and does not require treatment in addition to or beyond what is required by that standard.”[26]

The drafters added however a further provision which, while commendable for its sensitivity to varying host State conditions, may not assist in the endeavor to achieve greater legal certainty:

“3. For greater certainty, Member States understand that different Member States have different forms of administrative, legislative and judicial systems and that Member States at different levels of development may not achieve the same standards at the same time. Paragraphs 1 and 2 of this Article do not establish a single international standard in this context.”[27]

Within the 2012 Southern African Development Community Model Bilateral Investment Treaty, a note by the drafting committee records as follows:

“The fair and equitable treatment provision is, again, a highly controversial provision. The Drafting Committee recommended against its inclusion in a treaty due to very broad interpretations in a number of arbitral decisions. It requested the inclusion of an alternative formulation of a provision on ‘Fair Administrative Treatment.’”[28]

Two options are then set out. The first reads that “[e]ach State Party shall accord to Investments or Investors of the other State Party fair and equitable treatment in accordance with customary international law on the treatment of aliens,”[29] accompanied by the following specification: “For greater certainty, [the standard] requires the demonstration of an act or actions by the government that are an outrage, in bad faith, a wilful neglect of duty or an insufficiency so far short of international standards that every reasonable and impartial person would readily recognize its insufficiency.”[30] With these words, the drafters have captured essentially verbatim one of the most oft-quoted articulations of the deferential minimum standard in international jurisprudence, dating from the Neer Claim of nearly one hundred years ago.[31]

The precise contours of the minimum standard remain something less than fully demarcated, and this threshold remains oft-litigated even today. As such, even formulations such as these may not be fully effective in removing the indeterminacy that is characteristic of the standard nor in resolving the feature of most strident criticism.

A further option is to trend toward an independent standard detached from the international minimum, a more highly particularized prescription which might spell out a more precise meaning. The alternative formulation presented within the Southern African Development Community model treaty offers that “[t]he State Parties shall ensure that their administrative, legislative, and judicial processes do not operate in manner that is arbitrary or that denies administrative and procedural [justice] [due process] to investors of the other State Party or their investments [taking into consideration the level of development of the State Party.]”[32] Meanwhile in, for example, the Comprehensive Economic and Trade Agreement between Canada and the European Union and its member States, the parties have ascribed the following content to the FET standard:

“1. Each Party shall accord in its territory to covered investments of the other Party and to investors with respect to their covered investments fair and equitable treatment and full protection and security in accordance with paragraphs 2 through 7.

2. A Party breaches the obligation of fair and equitable treatment referenced in paragraph 1 if a measure or series of measures constitutes:

(a) denial of justice in criminal, civil or administrative proceedings;

(b) fundamental breach of due process, including a fundamental breach of transparency, in judicial and administrative proceedings;

(c) manifest arbitrariness;

(d) targeted discrimination on manifestly wrongful grounds, such as gender, race or religious belief;

(e) abusive treatment of investors, such as coercion, duress and harassment; or

(f) a breach of any further elements of the fair and equitable treatment obligation adopted by the Parties in accordance with paragraph 3 of this Article.

3. The Parties shall regularly, or upon request of a Party, review the content of the obligation to provide fair and equitable treatment. The Committee on Services and Investment, established under Article 26.2.1(b) (Specialised committees), may develop recommendations in this regard and submit them to the CETA Joint Committee for decision.

4. When applying the above fair and equitable treatment obligation, the Tribunal may take into account whether a Party made a specific representation to an investor to induce a covered investment, that created a legitimate expectation, and upon which the investor relied in deciding to make or maintain the covered investment, but that the Party subsequently frustrated.

5. For greater certainty, ‘full protection and security’ refers to the Party’s obligations relating to the physical security of investors and covered investments.

6. For greater certainty, a breach of another provision of this Agreement, or of a separate international agreement does not establish a breach of this Article.

7. For greater certainty, the fact that a measure breaches domestic law does not, in and of itself, establish a breach of this Article. In order to ascertain whether the measure breaches this Article, the Tribunal must consider whether a Party has acted inconsistently with the obligations in paragraph 1.”[33]

The States may now ascribe to their chosen treaty standards of investment protection any meaning they might wish in a forthcoming Africanization of international investment law.

Enforcing Investor Obligations

As for investor obligations, numerous of the substantive bases identified in the ARIA IX report are eminently viable candidates for inclusion, including in respect of human rights, labor rights, environmental rights, indigenous peoples’ rights and, of course, anti-corruption.[34] The proposed framework for balancing investor rights and States’ interests becomes meaningful where the investment protocol contains a mechanism to enforce the chosen investor obligations. On the issue of how to achieve jurisdiction over the investor in the arbitral forum, the authors of the ARIA IX report offer the following:

“Investor obligations

The international investment regime historically imposed obligations only on host States, not on private investors (Paulsson, 1995). However, as underscored by the PAIC, IIAs may serve as vehicles for investor rights and also for their obligations, which could rebalance the regime. Investor obligations can be a source for claims against transgressing investors and for counterclaims by defending States. The right to initiate proceeding may be bestowed upon the [host] State, its nationals or both (Amado, Kern and Rodriguez, 2017).”[35]

In similar vein, the UNCITRAL Secretariat has recorded that its Working Group III for Investor-State Dispute Settlement Reform “may wish to consider whether the framework for counterclaims by respondent States could be expanded to allow for claims by third parties against investors.”[36] Where desired, enhancements may be applied to the model of presently existing texts carrying investor obligations (such as in the RECs and the Pan-African Investment Code) to conclusively achieve obligations that are justiciable in international law.

In a first option, a contingent consent clause may be entered into the investment protocol, such that each host State’s standing offer of arbitration in respect of the investment protections is no longer unconditional but is rather contingent upon the investor giving his own consent to arbitration in respect of the chosen investor obligations:[37]

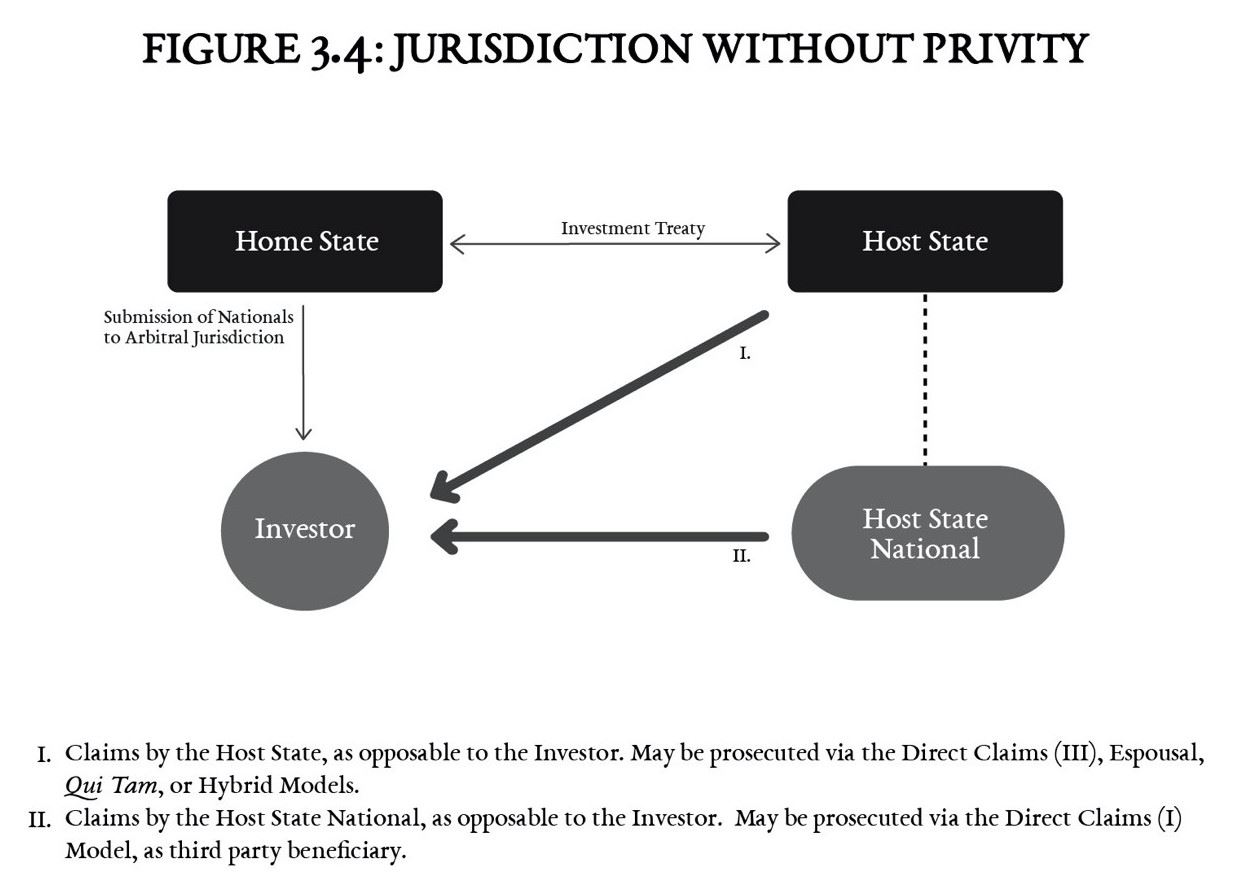

In a second option, jurisdiction over the investor may be obtained by direct effect of the investment protocol, with each State party acting to submit its own investor-nationals to the jurisdiction of an international tribunal by the simple fact of their effecting a cross-border investment, without need of their express consent, in a form of arbitration without privity:[38]

After all, in one of the very first treaty instruments to establish investor-State arbitration (and the first to confer jurisdiction upon the International Centre for Settlement of Investment Disputes), the Netherlands and Indonesia accorded in 1968 that “[t]he Contracting Party in the territory of which a national of the other Contracting Party makes or intends to make an investment, shall assent to any demand on the part of such national and any such national shall comply with any request of the former Contracting Party, to submit, for conciliation or arbitration, to [ICSID] any dispute that may arise in connection with the investment.”[39]

Conclusion

In conclusion, we propose a fair and equitable balance of investor rights plus countervailing investor obligations in international investment law. It has now been recognized that adoption of investor obligations is the right thing to do; in Africa, this debate is over. Further than this, in perhaps a rare instance, the normative motivation to do the right thing coincides with present practicality, for in this manner might one find the point of optimization and balance that may be acceptable to all. As a policy matter, such offers the viable pathway forward in negotiation of a mega-multilateral instrument with diverse capital importing and exporting interests present, both across and within the very many African States. At this time when the whole world casts about for a suitable model in the reform of international investment law, and at this time where we have placed our planet in peril, perhaps Africa might show the way by ensuring protections against true abuse of investors while also imposing hard investor obligations that will nurture the very most responsible business conduct, and thereby deliver what is truly a protocol on sustainable investment for Africa.

_____________________

*Of Counsel, Addis Law Group LLP co-authored by Gidey Belay Assefa of Addis Law Group LLP. The views herein expressed are those of the authors.

[2] Long prior to the emergence of the Pan-African Investment Code, investor obligations were seen in numerous instruments of the various regional economic communities. Early traces of investor obligations may be found in the 1980 Unified Agreement for the Investment of Arab Capital in the Arab States and the 1981 Agreement on Promotion, Protection and Guarantee of Investments Among Member States of the Organization of the Islamic Conference, to which some half of the States party are African. See Unified Agreement for the Investment of Arab Capital in the Arab States, 1980, available at https://investmentpolicy.unctad.org/international-investment-agreements/treaty-files/2394/download and Agreement on Promotion, Protection and Guarantee of Investments Among Member States of the Organization of the Islamic Conference, 1981, available at https://investmentpolicy.unctad.org/international-investment-agreements/treaty-files/2399/download. The 2006 Southern African Development Community Protocol on Finance and Investment requires investors to abide by the laws, regulations, administrative guidelines and policies of the host State. See Southern African Development Community Protocol on Finance and Investment, 2006, available at https://investmentpolicy.unctad.org/international-investment-agreements/treaty-files/2730/download. The 2007 Investment Agreement for the Common Market for Eastern and Southern Africa similarly requires investors to comply with all applicable domestic measures while expressly allowing for counterclaims by the host State (though it has never entered into force). See Investment Agreement for the Common Market for Eastern and Southern Africa, 2007, available at https://investmentpolicy.unctad.org/international-investment-agreements/treaty-files/3092/download. A 2008 Supplementary Act of the Economic Community of West African States introduces elements including investors’ obligations to conduct environmental and social impact assessments and to observe labor, human rights and corporate governance standards while expressly allowing the host State to raise a counterclaim or to initiate a unilateral claim opposable to the investor. See Supplementary Act of the Economic Community of West African States, 2008, available at https://investmentpolicy.unctad.org/international-investment-agreements/treaty-files/3266/download. These various provisions on investor obligations, while perhaps under-operationalized to date, are unmistakably present.

[3] Draft Pan-African Investment Code, December 2016, Article 42, available at https://au.int/sites/default/files/documents/32844-doc-draft_pan-african_investment_code_december_2016_en.pdf.

[4] See note 2 supra; see also, e.g., Reciprocal Investment Promotion and Protection Agreement Between the Government of the Kingdom of Morocco and the Government of the Federal Republic of Nigeria, 2016, available at https://investmentpolicy.unctad.org/international-investment-agreements/treaty-files/5409/download.

[5] Draft Pan-African Investment Code, December 2016, Articles 19-24, available at https://au.int/sites/default/files/documents/32844-doc-draft_pan-african_investment_code_december_2016_en.pdf.

[6] Won L. Kidane, Contemporary International Investment Law Trends and Africa’s Dilemmas in the Draft Pan-African Investment Code, The Geo. Wash. Int’l L. Rev. (2018) Vol. 50, 578.

[7] Draft Convention on Investments Abroad (Abs-Shawcross Draft Convention), 1959, available at https://www.international-arbitration-attorney.com/wp-content/uploads/137-volume-5.pdf.

[8] Treaty Between Federal Republic of Germany and Pakistan, 1959, available at https://investmentpolicy.unctad.org/international-investment-agreements/treaty-files/1387/download.

[9] See, e.g., M. Sornarajah, The International Law on Foreign Investment (Cambridge University Press, 3rd ed, 2010) 177.

[10] For a recent example of what may nonetheless be a significant success story in the domain of multilateral investment agreements, see Comprehensive and Progressive Agreement for Trans-Pacific Partnership, 2018, available at https://www.dfat.gov.au/sites/default/files/tpp-11-treaty-text.pdf. See also the China-led Regional Comprehensive Economic Partnership Agreement, 2020, available at https://investmentpolicy.unctad.org/international-investment-agreements/treaty-files/6032/download.

[11] OECD, Draft Multilateral Agreement on Investment, 1995, available at https://www.oecd.org/investment/internationalinvestmentagreements/multilateralagreementoninvestment.htm.

[12] Organisation of African Unity Charter, 1963, available at https://au.int/sites/default/files/treaties/7759-file-oau_charter_1963.pdf.

[13] Lagos Plan of Action for the Economic Development of Africa 1980-2000, Organisation of African Unity, 1980, available at https://www.uneca.org/itca/ariportal/docs/lagos_plan.pdf.

[14] Treaty Establishing the African Economic Community (with Protocol dated 2 March 2001), signed on 3 June 1991 (entered into force on 12 May 1994), available at https://treaties.un.org/doc/Publication/UNTS/No%20Volume/55375/Part/I-55375-0800000280526ec1.pdf.

[15] United Nations Economic Commission for Africa, How African countries are boosting intra-African investment, with a view to sharing best practices among member States (2017) 3.

[16] The Code, in its preamble, states that the member States recognize the “importance of trade and investments for the growth and development of Africa” and desire to “promote an attractive investment climate and expand trade and investment.” Draft Pan-African Investment Code, December 2016, Preamble, available at https://au.int/sites/default/files/documents/32844-doc-draft_pan-african_investment_code_december_2016_en.pdf. The protections and obligations that the Code extends are to African investors, and the presumed host states are the African states.

[17] Agreement Establishing the African Continental Free Trade Area, 2019, available at https://au.int/sites/default/files/treaties/36437-treaty-consolidated_text_on_cfta_-_en.pdf.

[18] United Nations Economic Commission for Africa et al, Assessing Regional Integration in Africa IX (2019) 187.

[19] On the right to regulate, see, e.g., Talkmore Chidede, The Right to Regulate in Africa’s International Investment Law Regime, Oregon Rev. of Int’l Law (2019) Vol. 20.

[20] For a fuller argument in favor of this proposition, see JD Amado, JS Kern and MD Rodriguez, Arbitrating the Conduct of International Investors (Cambridge University Press, 2018).

[21] Possible Reform of Investor-State Dispute Settlement (ISDS): Multiple Proceedings and Counterclaims, UN Doc. No. A/CN.9/WG.III/WP.193, dated 22 January 2020, available at https://undocs.org/en/A/CN.9/WG.III/WP.193.

[22] Resolution on Equality of Parties before International Investment Tribunals, Institut de Droit International, dated 31 August 2019, Preamble and Art. 2(1), available at https://www.idi-iil.org/app/uploads/2019/09/18-RESEN.pdf.

[23] Workplan to implement investor-State dispute settlement (ISDS) reform and resource requirements, UN Doc. No. A/CN.9/WG.III/WP.206, dated 21 March 2021, para. 9, available at http://undocs.org/en/A/CN.9/WG.III/WP.206.

[24] North American Free Trade Agreement, Notes of Interpretation of Certain Chapter 11 Provisions, NAFTA Free Trade Commission, 2001, available at http://www.sice.oas.org/tpd/nafta/commission/ch11understanding_e.asp.

[25] 2012 US Model Bilateral Investment Treaty, Art. 5 (“Minimum Standard of Treatment”), available at https://ustr.gov/sites/default/files/BIT%20text%20for%20ACIEP%20Meeting.pdf. An annex on interpretation states that “[t]he Parties confirm their shared understanding that ‘customary international law’ generally and as specifically referenced in Article 5 [Minimum Standard of Treatment] … results from a general and consistent practice of States that they follow from a sense of legal obligation,” and that “[w]ith regard to Article 5 [Minimum Standard of Treatment], the customary international law minimum standard of treatment of aliens refers to all customary international law principles that protect the economic rights and interests of aliens.” Ibid., Annex A.

[26] Investment Agreement for the COMESA Common Investment Area, 2007, Art. 14, available at https://investmentpolicy.unctad.org/international-investment-agreements/treaties/treaties-with-investment-provisions/3225/comesa-investment-agreement.

[27] Investment Agreement for the COMESA Common Investment Area, 2007, Art. 14, available at https://investmentpolicy.unctad.org/international-investment-agreements/treaties/treaties-with-investment-provisions/3225/comesa-investment-agreement (emphasis added).

[28] SADC Model Bilateral Investment Treaty Template, with Commentary, 2012, available at https://www.iisd.org/itn/wp-content/uploads/2012/10/SADC-Model-BIT-Template-Final.pdf.

[29] SADC Model Bilateral Investment Treaty Template, with Commentary, 2012, available at https://www.iisd.org/itn/wp-content/uploads/2012/10/SADC-Model-BIT-Template-Final.pdf.

[30] SADC Model Bilateral Investment Treaty Template, with Commentary, 2012, available at https://www.iisd.org/itn/wp-content/uploads/2012/10/SADC-Model-BIT-Template-Final.pdf.

[31] Neer Claim, Mexico-US General Claims Commission, RIAA, IV (1926) 61-62, available at https://legal.un.org/riaa/cases/vol_IV/60-66.pdf.

[32] SADC Model Bilateral Investment Treaty Template, with Commentary, 2012, available at https://www.iisd.org/itn/wp-content/uploads/2012/10/SADC-Model-BIT-Template-Final.pdf.

[33] Comprehensive Economic and Trade Agreement Between Canada, of the one part, and the European Union and its Member States, of the other part, provisionally entered into force on 21 September 2017, Art. 8.10 (“Treatment of investors and of covered investments”), available at https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A22017A0114%2801%29.

[34] See JD Amado, JS Kern and MD Rodriguez, Arbitrating the Conduct of International Investors (Cambridge University Press, 2018), Chapter 5. For a current inquiry into the anti-corruption basis identified in the ARIA IX report, see also JD Amado, JS Kern and MD Rodriguez, Elevating Corruption to an International Tort, in Investors’ International Law (J Ho and M Sattorova, eds.) (forthcoming 2021).

[35] United Nations Economic Commission for Africa et al, Assessing Regional Integration in Africa IX (2019) 198.

[36] Possible Reform of Investor-State Dispute Settlement (ISDS): Multiple Proceedings and Counterclaims, UN Doc. No. A/CN.9/WG.III/WP.193, dated 22 January 2020, available at https://undocs.org/en/A/CN.9/WG.III/WP.193 (emphasis added).

[37] JD Amado, JS Kern and MD Rodriguez, Arbitrating the Conduct of International Investors (Cambridge University Press, 2018) 87-90 and Annex, Model 6 (“Contingent Consent Clause”).

[38] JD Amado, JS Kern and MD Rodriguez, Arbitrating the Conduct of International Investors (Cambridge University Press, 2018) 90-93 and Annex, Model 7 (“Jurisdiction without Privity”).

[39] Netherlands-Indonesia Agreement on Economic Cooperation (with Protocol and Exchanges of Letters dated 17 June 1968), signed on 7 July 1968 (entered into force on 17 July 1971), 799 UNTS 13, Art. 11 (emphasis added), available at https://investmentpolicy.unctad.org/international-investment-agreements/treaty-files/3329/download.